5 The purchase-to-pay process

Let’s assume you’ve recently discovered the work of Cal Newport on time planning (and if you did not yet, then you should!). You are convinced that what he preaches is gold and you have decided to purchase The Time-Block Planner - A Daily Method for Deep Work in a Distracted World. You then go to your favourite web shop and purchase the Time-Block Planner. The joy! Imagine how productive you’ll be once you get that planner!

But your joy dissipates when you get an email with the text ‘We are writing to offer our heartfelt apologies for the delay in delivering your recent order for The Time-Block Planner. The unexpected surge in demand for the product you ordered, has caused a delay in restocking the item.’ What? How are you supposed to continue your work now?

What happened behind the scenes with the web shop? A first guess is that they had improper internal controls for the purchasing process, leading to a mismanagement of the inventory of Time-Block Planners. Do problems with the purchasing process appear only for web shop companies? Of course not. Let’s see another example below where the internal controls on the purchasing process failed.

I remember reading once that Warren Buffett, the renowned investor, loves to read annual reports of companies. Bill Gates describes in a 1996 Harvard Business Review article, ‘What I learned from Warren Buffett’, that, when Warren Buffett ‘invests in a company, he likes to read all of its annual reports going back as far as he can.’ Indeed, Warren Buffett’s flair for spotting valuable businesses made him rich and famous. Speed up to 2019 and we find out that Francine Mckenna, award-winner writer and teacher who migrated to investigative journalism after a career in the public accounting industry, is not so impressed with Warren

Mckenna’s 2019 article on Buffett’s investment company, Berkshire Hathaway, points out how the 2015 acquisition of Kraft by Heinz, and endorsed by Berkshire Hathaway was an investment mistake on Warren Buffett’s part. As it turns out, the year 2019 was a tumultuous year for the Kraft Heinz Co, the maker of Heinz Tomato Ketchup. Besides recording a record-making impairment loss of $15 400 000 000 ($15,4 billion), one of the largest in corporate history, the Kraft Heinz company also announced an internal investigation into its procurement process.

In an article titled ‘Kraft Heinz’s comeback begins after months of procurement scandal’ journalist Emma Cosgrove writes that, among other issues, ‘insufficient review of supplier contracts led to procurement misconduct’. We can think of ‘procurement’ as a fancy word for ‘purchasing’. Basically, Kraft Heinz’s team in charge of procurement did not uphold internal control requirements (e.g., did not check suppliers properly), and aggressively pushed to get the most profitable contracts, sometimes even taking advantage of complex supplier contracts to artificially reduce the cost of purchasing.

Why did I start this story with Warren Buffett? I’m not sure. I guess every story needs a villain. The overall conclusion is that internal controls on purchasing are needs for both web shops and food and beverages retailers.

5.1 Purchase-to-pay process

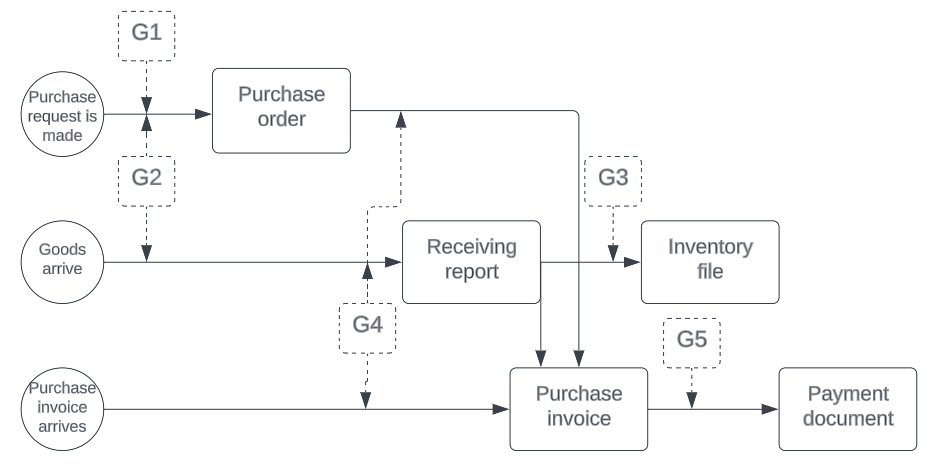

The purchase-to-pay process exemplified in Figure 5.1 has five organizational goals. Are there always only five organizational goals? No, there are more, but looking at five is a good start for getting the logic of diagrams and controls.

So what are our goals as an organization? We’ll look at the first information flow, from the purchase requisition to the purchase order. Our goal here (G1) is to purchase what we need, so the correct goods, at a price with which we agree. In order to achieve this goal we might think of preventive controls, such as the segregation of duties between the person who requests the goods and the person who purchases the goods. For example, in a restaurant, we might have the chef requesting specific goods with the purchase being done by another restaurant employee. If only one person employee would be responsible for purchasing, then he might purchase goods for his own use.

The arrow between the arrival of goods and the receiving report shows another flow of information. Here too, we would have a goal (G2): that the goods we receive are the actual goods we ordered, at the agreed prices. Continuing the restaurant example, if we ordered 50 bottles of Shiraz Rosé from Jacob’s Creek for €8,50 per bottle, then we need to make sure we actually receive this. So, we’ll perform an analytical review by checking the information on the purchase order (or what-should-be) against the information on the receiving report (or what-is).

The receiving report also updates the inventory file to reflect that now we have the goods. The goal here (G3) would be to only update the inventory file with correct information. So we could use a formal procedure where we only update the inventory file after the receiving report is checked against the purchase order.

When we receive an invoice, we’ll want to record it. Our forth goal (G4) is to only record invoices for the goods that we want and, in this case, also received. So we’ll check what we ordered (from the purchase order), with what we received (from the receiving report) with what was invoiced by the vendor (from the purchase invoice). This analytical review should give us confidence that we’re reaching our forth goal. Once we check all this information, we can approve the invoice (through a formal authorization procedure which dictates first the checking and then the approval) and only then we pay the invoice, reaching this way our fifth goal (G5) which is to only pay for goods ordered and received.

Did you follow along? Can you repeat the goals we had looking at the diagram? Do you remember where we used segregation of duties as a control activity? Do you remember what wine we ordered in our example?

So you see, for each flow of information (so for each arrow) we had to think of a control activity corresponding to an organizational goal. Is this diagram for the purchase-to-pay process set in stone? Of course not. After all, control is more of an art than a science. Also, each organization has their own processes. But you have some good building blocks now, knowing some ITPs (Information Transformation Points), some informational goals and some control activities connected to the purchase-to-pay process.

5.2 Questions and application:

- Can you describe an example of the purchase-to-pay process from real-life?

- Can you think of other goals that are missing from our exercise related to the purchase-to-pay exercise?

- Can you think of a different way in which the purchase-to-pay process can be structured?

- On what information flow would we check that the quality of the goods received is good enough?

- Discover how the purchase-to-pay process works in odoo.