6 The order-to-cash process

Have you ever sat on a Herman Miller office chair?

No?

Ok, no problem, the story works without you having to sit on a Herman Miller chair.

There is a book called ‘The Oz principle’. The authors, Roger Connors, Tom Smith, and Craig Hickman, write about the concept of individual and organizational accountability. Their overall message is that, in order to be effective, people and organizations should realize they are in control of their actions and that they should get away from the victim mindset. They advocate that instead of thinking ‘it’s so unfair that this happened; we cannot do/achieve this because of these colleagues and because of this boss and because of this teacher!’ 😉, we should think more in terms of ‘what can I do to make the situation better?’.

One example that they use in the book (and this is an old book!) is the situation Herman Miller experienced with shipping their furniture. Basically, each shipment of Herman Miller furniture contained a text outlining that ‘Damage [to the furniture] received during transit is the responsibility of the transportation company’. This is the victim mindset and the finger-pointing-‘it’s the other guy’s fault’-attitude that the Oz principle authors advocate against. Nevertheless, shortly after, the company took control of their actions and distanced itself from the blame game by changing the shipping notice text to contain ‘Call your Herman Miller dealer immediately. […] We are fully committed to your complete satisfaction.’ and continued to inform the customers of ways in which Herman Miller can support the customer if furniture becomes damaged during transport. This story links to the idea of not forgetting that we are always in control of something, even something as small as the smile on our faces.

Shipping is one part in the process of order-to-cash or, in order words, the sales process. In such a process, we start with a customer who wants to purchase something, we take these products from storage and we ship them and we make sure we receive money for the sale. Let’s see this in a diagram!

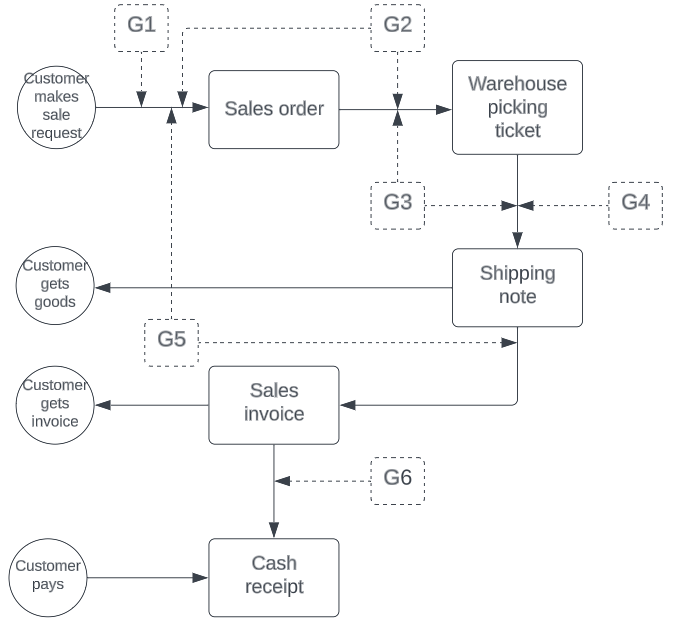

6.1 Order-to-cash process

The order-to-cash process is exemplified in Figure 6.1.

Have you studied a bit the diagram? Remember you can print the diagrams of this book from the fancy infographic - chapter 10 of this book. You can keep this infographic next to you while you read onwards about the goals of the organization for this process.

We’ll start with the first information flow, related to the arrow towards the sales order. Here, one goal (G1) would be that we sell to the right customers and not fictitious customers. So we’ll use a preventive control, a procedure, to check the creditworthiness of the customers.

Once customers are approved, we’ll want to make sure we pick up the right goods from the warehouse (G2). Here we can have another procedure where we only pick up goods which are in a sales order. We can also use a preventive segregation of duties by making sure that the person making the sales order is not the same person who is picking up the goods from the warehouse. Can you think of what can happen if the same person makes the sales order and also picks up the goods from the warehouse? That’s right! This person, could make up fake customers and fake sales orders and pick up the goods on her behalf.

So now we’ve piked up the goods from the warehouse. But picking up the goods is one thing and shipping them to the customer is another thing. Mistakes can intervene here when, despite picking up the right goods, we’re shipping the wrong ones to the customer. So, our goal is to ship the right goods to the customer (G3). When making the shipping note, we’ll use a procedure to check the sales order and the warehouse picking ticket. This way, we’re making sure that the goods from the sales order were picked up from the warehouse and are being shipped.

What else needs to happen when we take out goods from the inventory in order to deliver them to our customers? We need to update our inventory records. Our goal here is to have an updated inventory record (G4), otherwise our records will show we have goods which we actually don’t. Here we can think of the periodical control procedure of physical stock taking, where the information from the picking tickets is used to ascertain how much inventory we still have. So, if at the beginning of the period we have an inventory of 100 units and we have picking tickets for 80 units, then, when we physically count the inventory we should still find 20 units in our warehouse.

Our fifth goal (G5) is to invoice the right goods. Before creating a customer invoice, we’ll want to have a procedure that checks the sales order and the shipping note, to make sure that the goods ordered are actually shipped. Some years ago, it kept on happening that, whenever I purchased clothes online, I always received one or two extra items which were not in my order. I was invoiced for the goods I ordered and I did receive those, but I also was receiving one or two additional products I did not order. Where did things go wrong for my order? Let’s discuss in class.

Lastly, we also have the goal of receiving correct amounts as payment for the goods we delivered (G6). Here, an analytical review of checking the conformity between the sales invoice (what-is) and the bank statement information (what-should-it-be) would help.

For this order-to-cash process we followed a similar procedure as for the purchase-to-pay process. For each flow of information (for each black arrow) we had to think of a control activity (the dashed arrows) corresponding to an organizational goal (the dashed squares).

6.2 Questions and application:

- Can you describe an example of order-to-cash process from real-life?

- Can you think of other goals that are missing from our exercise related to the order-to-cash exercise?

- Can you think of a different way in which the order-to-cash process can be structured?

- Can you think of how stock-taking can go wrong?

- If we would want to add the fact that goods can be returned to the diagram, how would we do that?

- Discover how the order-to-cash process works in odoo.